October 13, 2025

A comprehensive introduction to the mechanics of covered calls within modern options markets. We examine how this strategy systematically generates income, its inherent risk-return profile, and its relevance for yield-focused portfolios.

Strategies in Derivatives trading often comes with complex structures and payoffs, which often prevents investors to get in touch with derivatives trading. However, looking into some of the strategies in more detail, it gets clear how powerful derivatives can be in a portfolio context. Especially looking at strategies around additional alpha generation of an existing underlying or finding the right entry point, options offer tremendous opportunities that no investor should ignore.

Two very basic and simple to understand strategies are “Cash Secured Put” and “Covered Call” strategies. Both strategies have the same payout function but are built for different purpose. Whereas the “Cash Secured Put” strategy is used to enter a position, the “Covered Call” Strategy is used to actively manage an existing position and generate additional income.

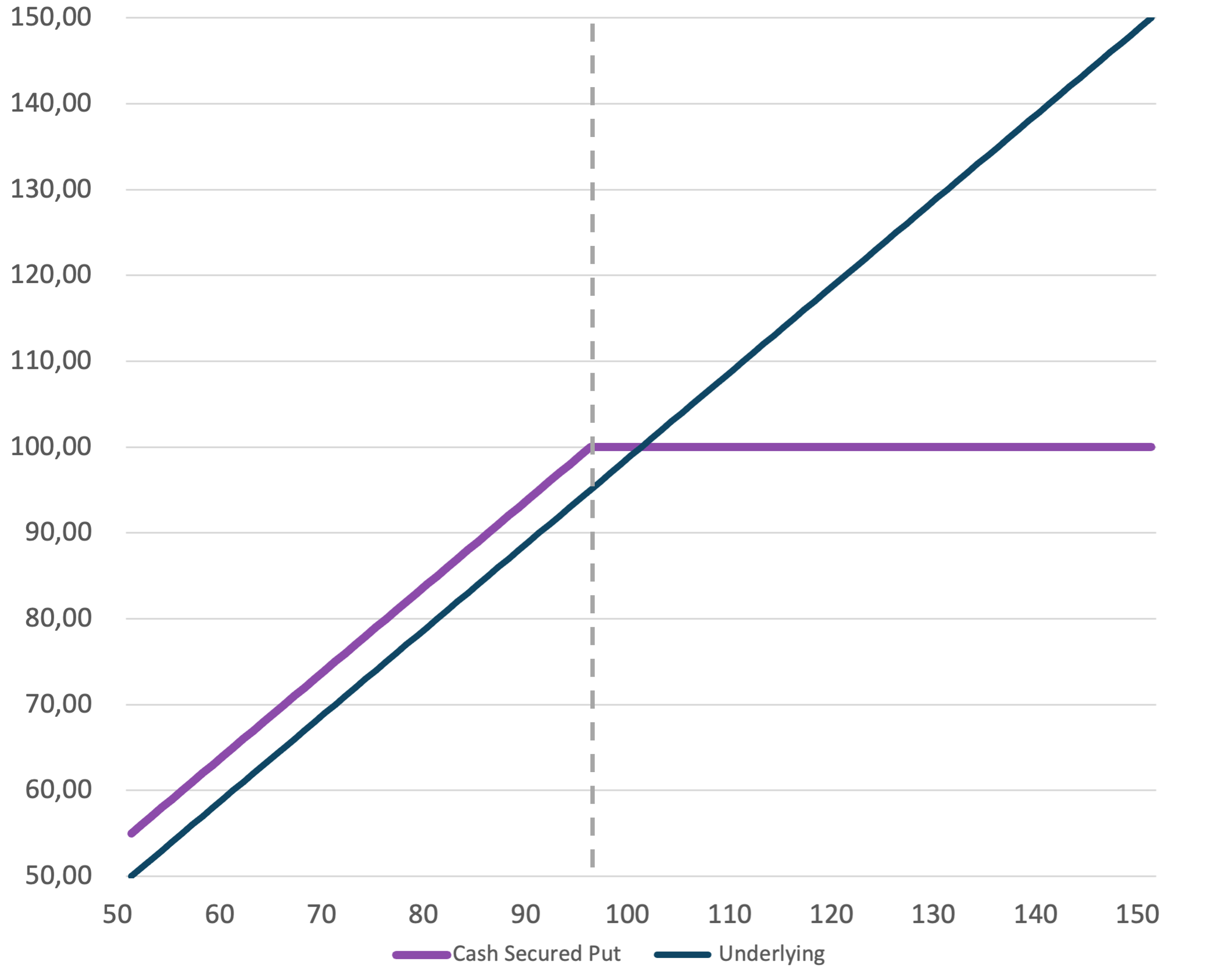

The “Cash Secured Put” strategy can be applied if you want to build a position in a certain underlying. Let’s assume a basic scenario of an underlying that is traded at a level of 100 USD. An investor has a positive view for the underlying asset and would be willing to buy if the underlying falls below 95 USD. Now he can either wait until the underlying reaches his entry level of 95 USD or he can actively start selling Put options with a strike price of 95 USD on this specific underlying. By selling the Put option, the investor is going into an agreement with another counterparty, let’s assume this is Investor B. Investor B is buying a Put option, because he wants to secure an existing position and with buying the Put options he has the right to sell the underlying asset at the price of 95 USD during a specified time period. To get this right, he will need to pay a premium to Investor A, seen like an insurance premium. Let’s assume in this example it is 5 USD. On the other side, Investor A has the obligation to buy the underlying at 95 USD during the specific time period, in case the underlying falls below 95 USD. To take that risk, he will receive the premium as a compensation. If the price will be at or above 95 USD, Investor A will collect premium and once the price falls below 95 USD, he will buy the asset but with the benefit of already collect premiums before that. The term “Cash secured” indicates the importance that the investor must secure the required cash aside to buy the asset, in this case the 95 USD.

The payout graph below shows the outcome of the strategy:

Covered Call Strategy results in a similar payoff, but the constituents differ to the Cash secured Put Strategy. Assume Investor A has bought the underlying with above strategy at 95 USD and he has the view that the underlying will increase but not skyrocketing. For that purpose, Investor A can sell a Call-Option on the same underlying. A Call Option gives an investor the right to buy a defined underlying at a certain price within a defined time period. Again, to buy this right, Investor B is willing to pay a premium. Because investor A owns the underlying, he can sell this option and collect the premium. Flipside of the coin is the obligation to deliver the underlying in case the option is exercised.

Let’s assume Investor A would be willing to sell a Call option with a strike price of 110 USD. In this case, he would not participate in any upside move above 110 USD and capping thereby his maximum payout until the expiry of the Call Option. As compensation he will receive the premium that Investor B is willing to pay to own the right to buy the asset at a price of 110 USD.

The payout graph below shows the outcome of the strategy:

Depending on the conviction of the view in an underlying asset, it is also possible to adjust the exposure to the Covered Call strategy. In case an investor still wants to participate in the upside with part of the exposure, the exposure to the covered call strategy can be reduced accordingly. In case of a reduction, let’s assume 75% of the exposure is subject to a covered call strategy and 25% is held as outright long position, the payout changes the following:

The profitability of the two strategies is highly dependent on the size of the premium received through the selling of the option. There are several factors influencing an options price, such as strike price, lifetime of the option, interest rates or dividend estimates in case of equity underlying's. Most important factor is, however, the so-called implied volatility. The implied volatility indicates the expected volatility during the lifetime of the option and is mainly determined by the expectation of market participants. It has nothing to do with the realized or historical volatility, but only what market participants are expecting in the future and are willing to pay.

The higher the expected volatility, the higher the option premium. Going back to our example of Investor A selling a call option and Investor B buying the call option, imagine that if there is big uncertainty where the price of the underlying at expiry of the option will be, Investor A will automatically expect a higher premium to take the risk of selling the underlying at the defined strike price. On the other hand, if the expectation or probability is near zero that he will be executed, he will not receive much for the option. Same is true for Put options, if there is high uncertainty in the market, Investor B will be willing to pay more for being hedged below 95 USD and limit his downside risk. In very calm market environments, he will be more willing being exposed to downside moves and respectively he will pay less for the insurance.

Whatever strategy is chosen and fits an investor need, one important element is to systematically stick to a defined strategy. Strategies often fail when markets go wild and emotions come into play. However, exact in such environments, markets often overshoot and offer income opportunities by sticking to an investment plan and strategy. Additionally, the re-investment of the premiums into the defined strategy is a key pillar of the long-term growth.

A comprehensive introduction to the mechanics of covered calls within modern options markets. We examine how this strategy systematically generates income, its inherent risk-return profile, and its relevance for yield-focused portfolios.

An overview of Bitcoin’s progression from a niche technological experiment to a globally recognized financial asset. We explore historical milestones, adoption dynamics, and its growing integration into institutional investment frameworks.

perspective on the development of the global ETP and ETF landscape. We analyze recent growth trends, the integration of cryptocurrencies within structured products, and how digital assets are shaping the future of exchange-traded markets.