September 25, 2025

An overview of Bitcoin’s progression from a niche technological experiment to a globally recognized financial asset. We explore historical milestones, adoption dynamics, and its growing integration into institutional investment frameworks.

Bitcoin was introduced in 2009 and is considered the first decentralized digital currency. Unlike conventional currencies such as the euro, Swiss franc, or US dollar, there is no central bank that issues or controls Bitcoin. Instead, the system is based on an open, global infrastructure: the blockchain.

The core idea of Bitcoin is to create a digital money system that operates independently of governments or banks. Participants can conduct transactions directly with each other without relying on intermediaries. This peer-to-peer principle makes Bitcoin globally accessible and transparent.

For investors, this means that Bitcoin is an asset not tied to national borders. Its value does not depend on the monetary policy of a particular country but solely on supply and demand in international markets.

A defining feature of Bitcoin is the absolute limitation of its supply. The code specifies that no more than 21 million units will ever exist. This limit cannot be altered and is enforced through the mechanism of mining: with each new block of transactions, new bitcoins are created, but their issuance is halved at regular intervals (the “halving”).

For investors, this artificial scarcity is highly relevant. While central banks can expand the supply of fiat currencies - for example, through bond purchases or interest rate cuts - the quantity of Bitcoin remains fixed. This makes Bitcoin resistant to inflationary expansion through political intervention.

The comparison to gold is obvious: gold is also limited, cannot be arbitrarily created, and has been used as a store of value for centuries. Bitcoin transfers this principle into the digital world - which is why it is often referred to as “digital gold.” In an environment of rising government debt and expansive monetary policy, scarcity can provide investors with a stabilizing factor.

In the traditional financial system, there are always central authorities that manage money: banks, payment providers, or governments. These structures have advantages but also risks. Bank accounts can be compromised by hackers, in some countries corruption undermines trust, and in times of crisis, governments can restrict access to deposits or block transfers. This means that control and security depend heavily on the institutions running the system.

Bitcoin works differently. There is no single bank or authority overseeing the money. Instead, a global network of thousands of computers runs the system. Each of these computers (a “node”) maintains a complete copy of the ledger - the list of all past transactions. New transactions are bundled together in blocks, and each block is cryptographically linked to the previous one. This forms the blockchain, a chain of blocks whose entries are practically immutable once confirmed.

Block confirmation is done through the proof-of-work process. In this process, miners compete against each other. Miners are computers in the network that provide their computing power to verify transactions and create new blocks. They solve complex mathematical problems, and whoever solves them first can add the next block and is rewarded with newly created bitcoins and transaction fees.

This process requires substantial computing power and energy but makes the network extremely resilient: to alter a confirmed transaction, an attacker would need to control more than half of the world’s computing power and simultaneously override all honest copies of the ledger. This is economically unfeasible.

For users, the system becomes visible through wallets. Each wallet has a unique address - comparable to a bank account number. On the blockchain, it is traceable which wallet address has sent funds to another. What is not visible, however, is who owns a particular address. This separation is known as pseudonymity. You can observe money flows between addresses, but the people behind them remain hidden unless they voluntarily reveal their wallet or connect it through a regulated exchange.

The history of Bitcoin begins in 2008 with Satoshi Nakamoto’s whitepaper, which first outlined a decentralized digital money system. In early 2009, the network launched with the so-called “genesis block,” laying the foundation for an entirely new type of financial system.

Initially, Bitcoin was known only in a small community. A landmark moment came in 2010 with the “pizza transaction,” when a programmer paid 10,000 bitcoins for two pizzas — the first documented real-world payment.

Since then, Bitcoin has evolved structurally. In 2017, the Chicago Mercantile Exchange (CME) introduced regulated Bitcoin futures, giving institutional investors access. Over the following years, professional custody solutions and a liquid options market were established. Another milestone was the approval of spot Bitcoin ETFs in the United States in 2024, significantly improving accessibility for a wide range of investors

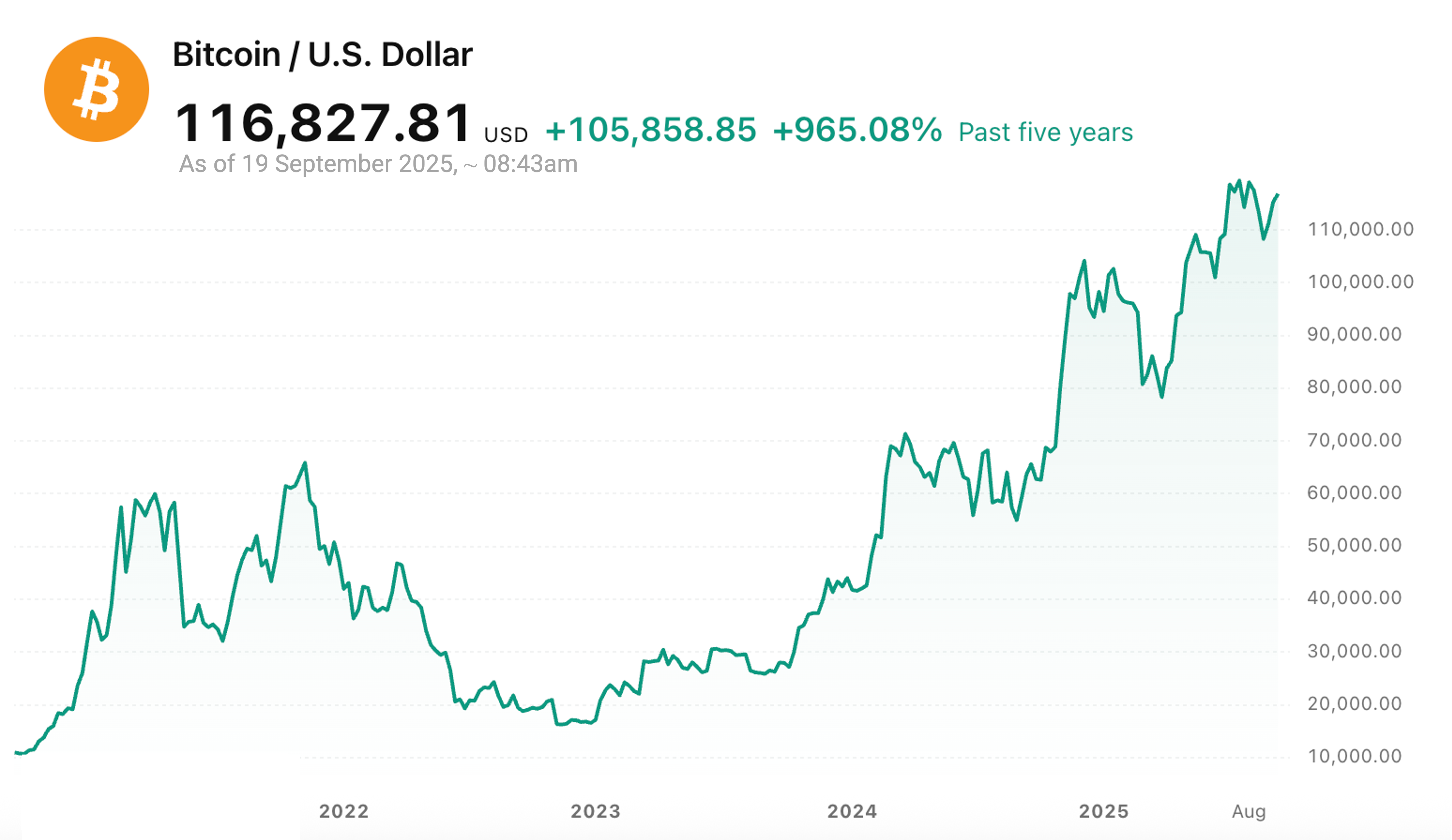

Bitcoin’s price has also developed strongly since its inception. After starting in the cent and dollar range, it broke through $1,000 in 2013, reached nearly $20,000 in 2017, and climbed to an all-time high of nearly $70,000 in 2021. Despite substantial volatility, this trajectory illustrates Bitcoin’s growing importance and market size over time.

Governments have also begun incorporating Bitcoin into their financial policies:

Bitcoin differs from traditional assets such as equities, bonds, or gold in several key ways. Its high volatility leads to substantial fluctuations but also creates opportunities not typically present in established markets. At the same time, Bitcoin has shown low long-term correlation with traditional assets, making it a potential diversifier.

For investors, this means Bitcoin can play a role as a portfolio addition. Even a small allocation may improve the risk-return profile, as Bitcoin’s price movements do not fully align with those of equities or bonds. The key is to size the allocation carefully, balancing potential benefits against risk tolerance.

In addition, the combination of high volatility and growing liquidity makes it possible to integrate Bitcoin into targeted strategies. Options are particularly relevant here:

From a professional perspective, Bitcoin is therefore suitable not only for passive buy-and-hold but also for systematic strategies that leverage its distinctive characteristics — high volatility, low correlation, and an increasingly mature market infrastructure.

A comprehensive introduction to the mechanics of covered calls within modern options markets. We examine how this strategy systematically generates income, its inherent risk-return profile, and its relevance for yield-focused portfolios.

An overview of Bitcoin’s progression from a niche technological experiment to a globally recognized financial asset. We explore historical milestones, adoption dynamics, and its growing integration into institutional investment frameworks.

perspective on the development of the global ETP and ETF landscape. We analyze recent growth trends, the integration of cryptocurrencies within structured products, and how digital assets are shaping the future of exchange-traded markets.